Why Card Chaos Never Announces Itself

Your corporate card policy for SMB operations probably looks fine on paper. Spending limits, category restrictions, receipt requirements, manager approvals above $500. Standard stuff.

Then month-end arrives and your controller spends three days chasing $47,000 in unreconciled transactions across 18 cards. Marketing bought software on personal cards because it was faster. Sales reps split large purchases to dodge approval thresholds. The facilities manager has 63 Amazon transactions described as "supplies" with zero documentation.

The problem isn't your policy document. It's the gap between what it says and what your systems actually enforce.

Why Card Policies Break Down in Growing Businesses

Cards get distributed to department heads to cut through purchase order bottlenecks. Makes sense—procurement moves faster, teams get what they need, finance stops being the gatekeeper on every $200 purchase.

But without enforcement, policy becomes optional. People find workarounds because those workarounds solve immediate problems. The sales director needs conference badges today. The operations manager sees a bulk discount expiring in two hours. The marketing lead's agency won't accept purchase orders.

Each exception looks reasonable in isolation. Together, they compound into reconciliation chaos. Your close stretches from 3 days to 7. Auditors flag control weaknesses. Your CFO can't trust expense reports without manual verification.

What makes this especially painful for SMB finance teams is scale. Not large enough to justify dedicated expense management headcount, but too complex for manual tracking. You're stuck where policy exists but enforcement requires heroic monthly effort.

The Real Cost of Manual Card Policy Enforcement

Most SMB finance teams underestimate what loose card policies actually cost. The obvious pain shows up during month-end close, but the operational damage runs deeper.

Stop letting accounting slow your business down.

Acctaly automates your financial operations so you can focus on growth and compliance.

- Automated bookkeeping

- Real-time financial reporting

- Integrated tax management

No credit card required

Consider a 35-person professional services firm with 12 corporate cards—executives, department heads, a couple of floaters for travel. Their stated policy requires receipts for everything over $25, manager approval above $500, and reconciliation by the 5th.

Reality: roughly $31,000 in monthly card spend with around 40% lacking proper documentation. The controller burns 16 hours a month chasing receipts. Department heads submit reconciliations whenever they get around to it, usually after multiple reminders.

The hidden costs keep stacking:

-

Duplicate subscriptions nobody catches for months

-

Unauthorized recurring charges that auto-renew

-

Personal expenses mixed with business spend

-

Vendor credits that never make it back to the company

-

Category violations that could trigger tax complications under audit

One logistics company found $8,400 in monthly duplicate software subscriptions across departments. Different managers bought the same tools because nobody had visibility into existing licenses. That's over $100,000 annually in pure waste, only discovered because a new CFO did a line-by-line review during budget season.

Role-Based Templates That Match Real Organizational Structures

Generic card policies fail because they ignore how organizations actually operate. Your sales team's spending patterns look nothing like your development team's. Remote employees face different expense realities than headquarters staff.

Effective policies start with role-based templates built around operational reality.

Executive Cards

Executives need flexibility but not carte blanche. Higher limits, but documentation requirements for investor relations and board reporting. Auto-flag entertainment expenses over $1,000. Require a second signature on any vendor contract initiated via card payment. Block certain merchant categories entirely—gambling, adult entertainment, cryptocurrency exchanges.

Department Lead Cards

Department heads typically manage team purchases and subscriptions. Monthly limits tied to approved budgets. Recurring charges restricted to pre-approved vendors. Itemized receipts required for transactions that could split across projects or cost centers. Auto-decline outside normal business hours unless pre-approved for conferences or travel.

Project Cards

Temporary cards for specific initiatives need tight controls. Expiration dates matching project timelines. Merchant categories limited to what's relevant. Project codes required on every transaction. Auto-suspend when project milestones are missed. Weekly spend reports going directly to project managers.

Travel Cards

Travel spending follows predictable patterns with predictable violations. Daily limits for meals and accommodation based on destination. Cash advances blocked over $200. Any travel expense without a corresponding calendar entry or trip approval gets flagged. Receipts required on everything, not just transactions over $75.

These aren't just policy documents. They're configuration templates that flow directly into your card issuance and expense management systems—and that distinction matters more than most people realize.

Automated Enforcement Rules That Prevent Violations Before They Happen

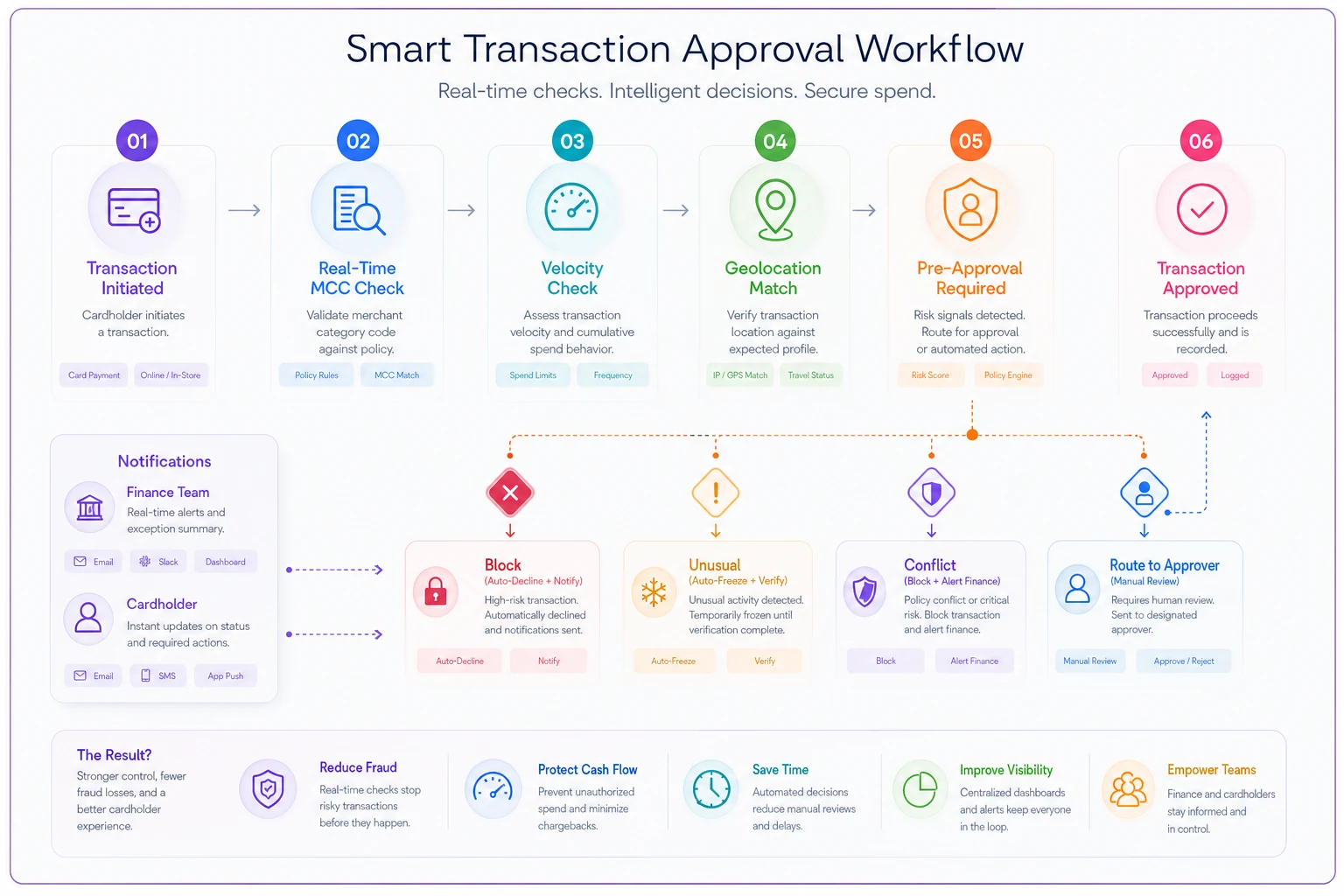

Policy without enforcement is wishful thinking. Manual enforcement burns hours without actually preventing problems. You need controls that operate continuously, not just during monthly reviews.

[Transaction Initiated] ↓ [Real-Time MCC Check] → Block? → [Auto-Decline + Notify] ↓ [Velocity Check] → Unusual? → [Auto-Freeze + Verify] ↓ [Geolocation Match] → Conflict? → [Block + Alert Finance] ↓ [Pre-Approval Required?] → Yes → [Route to Approver] ↓ [Transaction Approved]

A quick visual makes the enforcement flow easier to implement.

Real-time merchant category blocks stop problems at the point of sale. If your policy prohibits personal software subscriptions, block consumer software merchants at the processor level. When someone tries to charge a personal Spotify account, the transaction fails immediately—no receipt chase, no awkward conversation, no violation to unwind.

Transaction velocity controls catch unusual patterns early. Normal corporate card usage has rhythms. When a card processes 15 transactions in two hours, something's off. Either the card is compromised or someone's padding expenses. Auto-freeze and require verification.

Geolocation matching adds another layer. If a card processes a transaction in Miami while the cardholder's calendar shows them in Seattle, you have a problem. Shared card details or a compromised card—either way, the transaction blocks automatically while finance and the cardholder both get notified.

Pre-approval workflows eliminate ambiguity on specific categories. Any software subscription over $100/month requires IT sign-off before the card activates for that merchant. Conference registrations need budget confirmation. International transactions require travel authorization. The card simply won't work without proper approvals in place.

Exception Workflows That Handle Edge Cases Without Breaking Controls

Rigid policies create their own problems. Sometimes the CEO needs to pay an emergency vendor. Sometimes travel plans change mid-trip. Sometimes a critical purchase happens at 11pm.

Exception workflows preserve control while enabling necessary flexibility. The key is keeping exceptions traceable, documented, and reviewable—not just allowed.

| Transaction Type | Primary Approval | Escalation Path | Documentation Required | Review Frequency |

|---|---|---|---|---|

| Over-limit purchase | Direct manager | Department head → CFO | Business justification, quote, budget impact | Weekly |

| New software subscription | IT manager | CTO → CFO | Vendor assessment, license count, integration plan | Monthly |

| After-hours transaction | Auto-approved if under $200 | Manager → Finance | Receipt within 24 hours | Daily |

| International charge | Pre-approval required | CEO approval for urgent | Travel authorization, trip purpose | Per transaction |

| Merchant category override | Not allowed | CFO only | Written justification, temporary timeline | Monthly |

Exception requests should route through mobile notifications, not email threads. When someone's standing at a vendor counter needing approval, a 48-hour email chain doesn't work. Push notification to manager, five-minute response window, automatic escalation if no response.

Track exception patterns over time. If marketing requests software subscription exceptions every week, your pre-approved vendor list needs updating. If sales consistently hits travel limits during conference season, your seasonal calibration is off.

Monthly Review Routines That Catch What Automation Misses

Even solid automated controls need human oversight. Not everything translates to rules. Some patterns only become visible in aggregate, and some violations technically follow policy but violate common sense.

Structure monthly reviews as operational audits, not just reconciliation exercises. Start with automated exception reports—every override, every escalation, every pattern breach. Three manager overrides on the same vendor suggests your approved vendor list needs updating. Multiple after-hours exceptions from the same person could indicate workload problems or something more deliberate.

Review velocity patterns by department. A sudden spike in IT equipment purchases might signal project needs nobody communicated to finance. Declining travel expenses could indicate sales pipeline problems before they show up in revenue numbers.

Compare actual spending against assigned categories too. Merchant category codes aren't perfect. That "office supplies" charge might be a client dinner. The "computer equipment" transaction could be personal electronics. Manual review catches what automation doesn't.

Audit documentation quality, not just existence. A receipt that reads "various items - $847.32" technically meets the receipt requirement but provides zero actual control. Flag these for follow-up.

Tying Card Policy Directly to Reconciliation Quality

The best corporate card policy connects spending controls to reconciliation outputs. When policies exist in isolation, compliance stays optional. When policy violations directly affect reconciliation, people pay attention.

Map every transaction to your chart of accounts automatically. No more generic "credit card expense" line items. That Amazon purchase splits between office supplies, computer equipment, and training based on what was actually bought—and this granularity happens at transaction time, not during month-end scrambles.

Implement reconciliation scoring that tracks documentation quality. Complete receipt with business purpose noted? Full points. Missing receipt but under policy threshold? Partial credit. Consistent pattern of missing documentation? Escalation triggered.

Create feedback loops between reconciliation issues and policy enforcement. When someone consistently submits poor documentation, their real-time controls tighten—lower transaction limits, more categories requiring pre-approval, additional documentation requirements. Make good behavior easier than cutting corners.

This shifts reconciliation from a compliance exercise to an improvement tool. Each close provides data for next month's controls. Clean reconciliation becomes self-reinforcing—better documentation enables smoother closes, which frees time for proactive control work rather than firefighting.

Building Exception Triage Systems That Scale

As transaction volumes grow, manual exception review gets unwieldy. You need systematic triage that routes issues based on risk and materiality.

Start with automated risk scoring. A $50 policy violation from a trusted five-year employee rates differently than a $500 exception from someone hired last month. Multiple small violations from the same person score higher than one large exception with proper approval. Pattern violations—same merchant, same amount, same day each month—suggest systematic issues.

-

Low risk, low value — Auto-approve with documentation requirement

-

Low risk, high value — Manager review within 24 hours

-

High risk, low value — Finance review within 48 hours

-

High risk, high value — Immediate escalation to CFO

Build pattern recognition into your triage logic. Three employees suddenly buying from the same new vendor could indicate a legitimate business need nobody flagged—or coordinated policy gaming. Multiple declined transactions from approved vendors might mean credit line issues. Unusual timing patterns, like everything purchased on the last day of the month, could signal budget manipulation.

Your triage logic should evolve from outcomes. Exceptions that repeatedly get approved should trigger policy reviews. Violations that consistently get rejected might need clearer communication or tighter controls upfront.

The Compound Effect of Consistent Enforcement

Most SMB finance teams treat corporate card management as compliance overhead that adds no real value. But well-automated card policy enforcement creates compound operational benefits that go well beyond expense reports.

Consistent enforcement reduces resentment. When everyone follows the same rules, the "finance bureaucracy" complaints disappear—especially when executives go through identical approval processes. New employees learn faster when systems guide behavior instead of relying on tribal knowledge passed through Slack messages.

Predictable reconciliation frees up strategic capacity. When your close happens reliably by day 3, you gain several days monthly for actual analysis. Finance shifts from chase-and-reconcile mode to proactive guidance—spotting trends, preventing problems, rather than just documenting them after the fact.

Clean expense data improves every downstream process. Accurate department allocations make budgeting realistic. Proper categorization keeps tax compliance straightforward. Complete vendor information enables spend analysis and gives you negotiation leverage you wouldn't otherwise have.

One marketing agency implemented automated card policy enforcement and went from 8-day closes to 3-day closes within six months. First-time documentation compliance hit 94%, and they found over $6,000 monthly in reducible subscription spend just from having clean, categorized data to actually look at.

When Automated Card Policies Make Sense (and When They Don't)

Not every SMB needs sophisticated card policy automation. Under 10 employees with two or three cards, manual controls probably suffice. But certain situations signal when automation becomes necessary.

You need automated enforcement when:

-

Month-end reconciliation regularly extends past day 5

-

Card count exceeds 5 or monthly spend exceeds $20,000

-

You're facing audit findings about control weaknesses

-

Multiple departments issue their own cards independently

-

Remote work makes receipt collection difficult

-

You're planning significant headcount growth

You're probably not ready if:

-

Your entire team shares one or two cards

-

Monthly spend stays under $5,000

-

You have no dedicated finance person

-

Your business model requires maximum spending flexibility

The middle ground often works best: basic automation for routine controls, human oversight for exceptions. Auto-block certain merchants, require receipts through mobile upload, keep approval workflows simple. Add sophistication as complexity grows.

Implementation Checklist for Immediate Improvements

Building comprehensive automated card policies takes time, but several things can start immediately:

-

Create role-based card profiles — Map every card to a specific role with defined limits and restrictions. Start with three templates: executive, department head, and general user.

-

Configure merchant category blocks — Identify 5–10 merchant categories your business never needs. Block them at the processor level today.

-

Set up mobile receipt capture — Require photo uploads within 24 hours of purchase. Modern expense apps make this trivial, and it stops the receipt chase problem immediately.

-

Implement transaction notifications — Every cardholder and their manager should get real-time transaction alerts. Transparency alone improves compliance noticeably.

-

Build a simple exception log — Even a shared spreadsheet beats nothing. Track every override, who approved it, and why. Review patterns monthly.

-

Create monthly reconciliation deadlines — Set automated reminders at day 3, 5, and 7. Suspend cards at day 10 for non-compliance. Make deadlines real.

-

Generate automated spending reports — Weekly summaries by department, monthly trends by category. Visibility drives behavior change.

-

Document your actual policy — Not what you wish happened, but what actually happens. Build automation from reality, not theory.

Start with three role templates—executive, department head, and general user—to get immediate wins.

Corporate card policy for SMB operations doesn't have to be a monthly nightmare.

From Manual Chase to Systematic Control

The gap between policy and practice closes when you embed controls directly into operational workflows. Automation handles routine enforcement. Exceptions get documented and reviewed. Reconciliation becomes a validation exercise instead of an investigation.

The transformation is gradual. Start with basic controls—merchant blocks and receipt requirements. Add approval workflows as patterns emerge. Build exception handling as edge cases appear. Layer in analytics once base processes stabilize.

The businesses that get this right stopped treating card policy as a compliance checkbox and started viewing it as operational infrastructure. When systems enforce good behavior automatically, reconciliation hygiene becomes the natural outcome rather than the monthly struggle.

The businesses that get this right stopped treating card policy as a compliance checkbox and started viewing it as operational infrastructure. When systems enforce good behavior automatically, reconciliation hygiene becomes the natural outcome rather than the monthly struggle.

Ready to take control of your finances?

Join over 2,000 businesses using Acctaly to simplify accounting, accelerate cash flow, and ensure tax readiness.