Most founders waste three to four weeks assembling investor diligence packs because they're drowning in conflicting advice. VCs ask for everything, lawyers suggest 60+ documents, and some startup blog you read last month recommended building a full data room before you've even taken investor calls.

A scenario that plays out more than people admit: a 15-person B2B SaaS company finally hitting real traction—call it $80k MRR—gets three investors who want to move forward. The diligence requests come in and they look like procurement audits for a Fortune 500 acquisition. The founder scrambles to create documents that don't exist, pulls reports their accounting system can't generate, and starts writing policy narratives for things they've never formalized. Deals die from momentum loss, not missing paperwork.

Why Traditional Diligence Lists Kill Deal Momentum

The standard investor-ready diligence checklist you find online assumes you're raising Series B with a full finance team, legal counsel on retainer, and clean books going back five years. These lists originated from later-stage M&A processes and got copy-pasted down to seed rounds where half the items literally cannot exist yet.

Founders who close quickly provide exactly what investors need to make a decision at their current stage—nothing more. A seed investor evaluating a $2M round needs fundamentally different proof points than a growth investor writing a $15M check.

The real damage comes from over-delivering. Creating unnecessary documentation doesn't just waste time—it surfaces gaps that wouldn't have mattered otherwise. That detailed IP assignment tracker you built? Now they're worried about a contractor from 2021. The five-year projection model? Suddenly they're questioning year-four assumptions you pulled from thin air at 11pm.

Stage-Specific File Lists That Actually Close Deals

Pre-Seed / Friends & Family ($100k–$500k)

Stop letting accounting slow your business down.

Acctaly automates your financial operations so you can focus on growth and compliance.

- Automated bookkeeping

- Real-time financial reporting

- Integrated tax management

No credit card required

At this stage, investors are betting on you and the problem. Operational perfection is irrelevant. Your entire diligence pack should be five or six files:

Core Documents:

-

Formation docs (certificate of incorporation, bylaws)

-

Cap table (a simple spreadsheet showing who owns what)

-

Bank statements (last 3 months)

-

Basic P&L (monthly for whatever history you have)

-

Founder agreement (if there are multiple founders)

Reconciliation needed: Prove the bank balance matches your reported cash. That's genuinely it.

One thing to prepare a narrative for: If you're pivoting from a previous idea, write two paragraphs explaining what you learned and why the new direction makes sense. Don't hide it—they'll find out anyway, and hiding it reads worse than the pivot itself.

Seed Round ($500k–$2M)

Now investors want some evidence of early traction and clean fundamentals. Aim for somewhere around 10–12 files total, not a comprehensive dossier.

Financial Documents:

-

Monthly P&L (12 months or since inception, whichever is shorter)

-

Current balance sheet

-

Bank statements (6 months)

-

AR aging report (if relevant to your model)

-

Monthly metrics dashboard showing cohort retention

Legal Documents:

-

All formation docs

-

Current cap table with option pool

-

Employment agreements (founders and key employees)

-

Customer contracts (top 3–5 only)

-

Any convertible notes or SAFEs

Reconciliation priorities: Revenue recognition if you have annual contracts, and basic cash-to-bank reconciliation.

Common red flag that needs a narrative: Customer concentration. If one customer is over 30% of revenue, draft a brief explanation of expansion plans and what the pipeline looks like beyond them.

Series A ($3M–$10M)

Growth investors need proof of repeatability. This is where you finally need real diligence materials—but you can still keep it under 25 documents if you're disciplined.

Financial Package:

-

24 months of monthly financials

-

Detailed revenue build (by customer, cohort, or product line)

-

Budget vs. actual for current year

-

Unit economics breakdown

-

Cash flow statement (monthly)

-

All bank and credit card statements (12 months)

Operational Documents:

-

Sales pipeline snapshot

-

Churn analysis with reasons

-

Product roadmap (next 6 months only—anything beyond that is speculation anyway)

-

Org chart with comp ranges

-

Key vendor agreements

Legal/Compliance:

-

All investment documents from previous rounds

-

IP assignments from employees and contractors

-

Litigation history or threats

-

Material customer contracts

-

Insurance policies summary

Critical reconciliations: Revenue to cash collections, deferred revenue rollforward, and equity to cap table.

The difference between a Series A pack that moves quickly and one that stalls is usually just how well the numbers connect to each other. Investors will trace revenue back to bank statements. If that trail requires three emails and a spreadsheet explanation, you've already slowed things down.

Narratives for the Stuff Investors Always Ask About

Most founders write these reactively—after an investor flags something uncomfortable at 9pm the night before a partner meeting. Write them proactively instead.

These aren't fill-in-the-blank templates. They're starting points. The founders who use narratives most effectively are the ones who add specific context—actual dates, real dollar amounts, names of the people involved. Generic explanations read as evasive even when the underlying situation is completely fine.

When you changed accounting methods:

Explain what changed, when, and roughly what impact it had on recognized revenue. If you moved from cash to accrual, say so plainly. Investors have seen this before. What they're checking for is whether you understand what happened and whether the go-forward reporting is clean.

When burn spiked:

One founder had a month where burn jumped around 60% with no explanation anywhere in the documents. Turned out it was a planned engineering hire ahead of a product launch—totally reasonable—but hours of diligence went toward reconstructing it from bank statements. A two-sentence note would have prevented all of it. Write what drove the increase, whether it was planned, and what current burn looks like.

When historical records are incomplete:

This is more common than people admit. A lot of early-stage companies did their bookkeeping in spreadsheets, or in a system they later migrated away from, or with the help of a part-time bookkeeper who has since moved on. Be clear about what you have, what you reconstructed and how, and where the clean record-keeping starts. Trying to paper over gaps never works.

When one customer is most of your revenue:

Name them (under NDA if needed), state the contract terms, explain the renewal dynamics, and then show what the pipeline looks like beyond them. The goal isn't to minimize the concentration—it's to show you understand the risk and have a real plan.

When founder equity is uneven:

Explain why it was structured that way at the time. Usually there's a legitimate reason—one founder was full-time while the other had a day job, or one put in capital, or roles shifted during early development. Investors aren't looking for perfect 50/50 splits. They're checking for unresolved tension or surprise cliffs that could blow up after a check is written.

Red Flags That Need Proactive Narratives

Revenue Recognition Inconsistencies

If you've been recognizing annual contracts entirely upfront—which is extremely common at early stages—fix it before diligence starts. Create a simple reconciliation showing the adjustment and implement deferred revenue tracking going forward. Don't try to bury it. Experienced investors will spot it immediately in your cash flow patterns.

Informal Advisor Equity Grants

Those verbal promises for 0.5% equity? Document them or explain why they won't be honored. Deals have cratered over undocumented equity promises that materialized mid-diligence. Either formalize the agreements or have a clear explanation ready.

Interstate Sales Tax Exposure

Operating across state lines without proper sales tax registration is basically universal among early-stage companies. Calculate your actual exposure—it's usually smaller than founders fear—register in your top states by revenue, and put together a brief note on your compliance plan. Most investors understand this if you show you're actively addressing it rather than hoping no one notices.

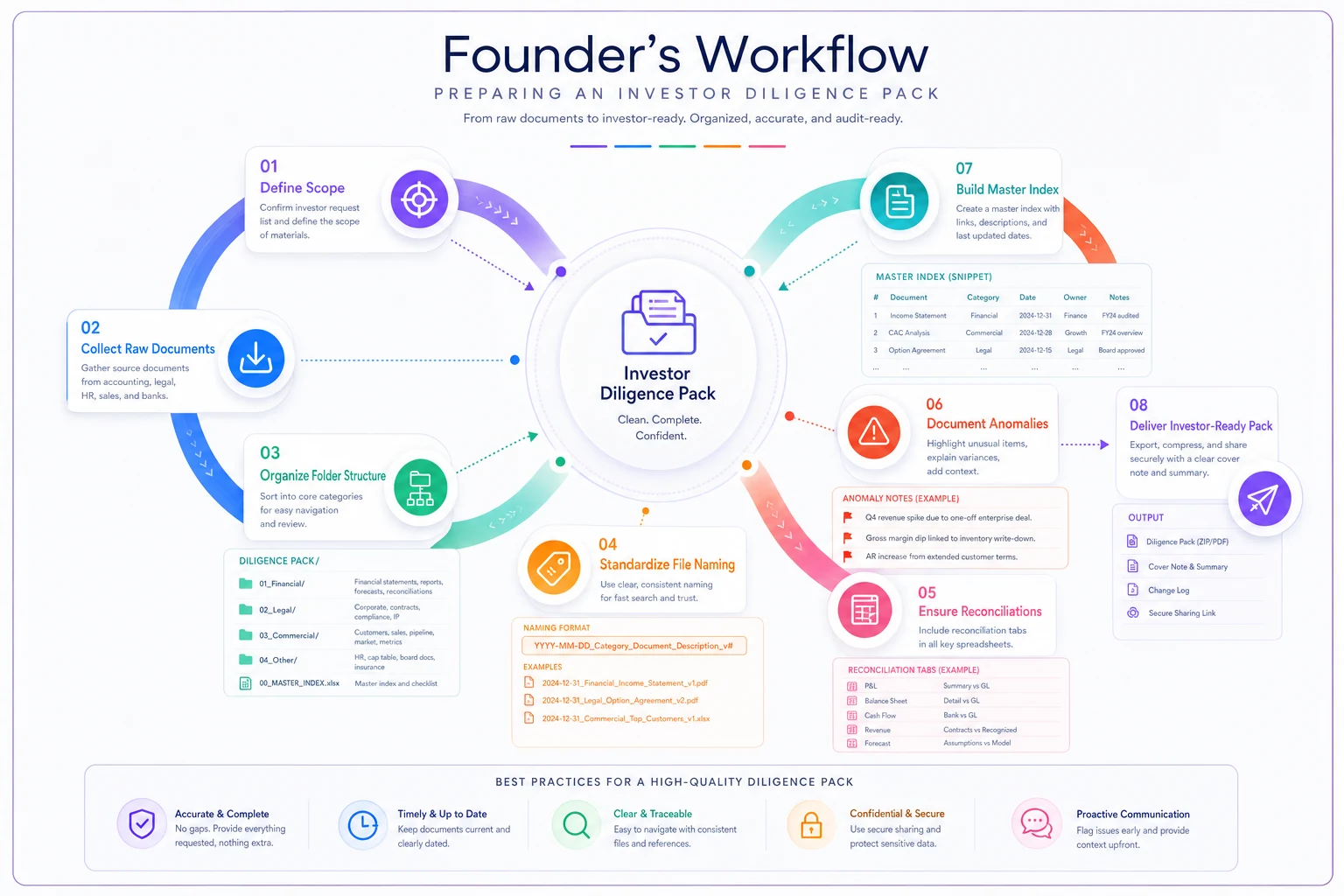

Building Your Pack with Minimal Back-and-Forth

The fastest diligence processes happen when founders anticipate questions before they're asked. Instead of sending raw documents that generate 40 follow-ups, add cover sheets with context. Your monthly P&L should include notes on anomalies. Your cap table should show fully diluted ownership clearly. Your customer list should note contract terms and renewal dates.

A workflow that actually holds up in practice:

-

Create a simple folder structure matching investor categories (Financial, Legal, Commercial)

-

Name files with dates and clear descriptions—"2024-10MonthlyP&L.pdf" not "financesv3FINAL.pdf"

-

Include a master index listing all files with one-line descriptions

-

Add reconciliation tabs to any spreadsheet where numbers need to tie together

-

Write brief notes on anything unusual before they ask

Here's a quick reference for what each stage actually requires:

| Stage | Total Files | Key Reconciliation | Primary Narrative Risk |

|---|---|---|---|

| Pre-Seed | 5–6 | Bank to cash | Pivot history |

| Seed | 10–12 | Revenue recognition, cash-to-bank | Customer concentration |

| Series A | Up to 25 | Revenue to collections, deferred revenue, cap table | Churn drivers, burn spikes |

Maintaining a reasonably investor-ready pack throughout the year is far less painful than scrambling during an active raise. Update monthly financials as part of your close process. Keep contracts organized. Maintain the cap table properly after every option grant.

AI-powered operational software makes this significantly easier—when contracts, financials, and operational data live in one system, producing diligence materials becomes a matter of running reports rather than hunting through email threads and folders named "OLDdontuse."

This visual shows the practical steps in the workflow above.

Include a master index with file descriptions and dates so every investor can see where to find supporting evidence quickly.

Maintaining the pack and treating it as part of your regular close process reduces frantic, last-minute work and preserves deal momentum when you go out to raise.

The Psychology of Clean Diligence

Investors aren't looking for perfection. They're looking for awareness and control.

A founder who proactively explains their customer concentration risk comes across better than one with perfect distribution who seems oblivious to other problems. The narrative often matters more than the actual numbers, especially at early stages.

What kills deals isn't the problems themselves—it's the surprises. That contractor you paid in equity without paperwork? Not a deal killer if you disclose it upfront with a remediation plan. Buried in hour three of diligence? Now they're wondering what else isn't documented.

Start With the Minimum, Add Only What's Asked For

The right investor-ready diligence pack depends entirely on your round size and where the business actually is. Over-preparing wastes weeks and frequently creates more concerns than it resolves. Under-preparing kills momentum when investors can't get basic questions answered.

Start with the minimum viable pack for your stage. Add documents only when specifically requested. Put your energy into honest, clear narratives for real issues rather than trying to bury them in polished paperwork.

When you get this balance right, what typically takes four to six weeks of back-and-forth compresses into something closer to a week or ten days of focused execution. That momentum difference is often the margin between closing the round and watching it slowly die from process fatigue.

When you get this balance right, what typically takes four to six weeks of back-and-forth compresses into something closer to a week or ten days of focused execution. That momentum difference is often the margin between closing the round and watching it slowly die from process fatigue.

Ready to take control of your finances?

Join over 2,000 businesses using Acctaly to simplify accounting, accelerate cash flow, and ensure tax readiness.