Every small business plays the same exhausting game with accounts payable. Bills pile up, payment terms conflict, and someone makes daily judgment calls about who gets paid first. The accounting team processes everything the same way — a $50 office supplies invoice gets the same treatment as a $15,000 inventory order. Meanwhile, cash sits idle when you could be capturing early-payment discounts, or worse, you're burning through reserves paying vendors who would've happily waited another 30 days.

The real problem isn't late payments or angry vendors. It's that most SMBs run accounts payable like they're still a five-person startup. No vendor segmentation. No payment routing logic. No automated approval workflows. Just a pile of invoices, manual decisions, and missed opportunities to optimize working capital.

The fix is building a working capital AP strategy that SMB operations can actually execute. Not some corporate procurement playbook — a practical system that segments vendors, automates routing decisions, and preserves cash without damaging vendor relationships.

Why standard AP processes destroy working capital

Most businesses inherit their AP process from whoever set up QuickBooks on day one. Invoices arrive, someone enters them, the owner approves everything over $500, and payments go out whenever cash looks decent. This works fine until you hit maybe 15 vendors or somewhere around $50,000 in monthly payables.

Then the cracks show up.

Your biggest supplier offers 2% net-10 terms on a $12,000 monthly order, but nobody catches it because the invoice gets processed with everything else. That's $240 monthly left on the table — almost $3,000 a year. Meanwhile, you rush to pay a marketing agency that explicitly offers net-60 terms because their invoice happened to land during a cash-heavy week.

The manual approval bottleneck creates its own headaches. The CEO reviews every significant invoice, which sounds responsible until they're traveling and a critical vendor payment sits for a week. Or the opposite — rushed approvals lead to duplicate payments because nobody has time to cross-check against previous invoices.

Working capital suffers from both directions. You miss the window to hold cash longer with flexible vendors. You miss discounts from strategic suppliers. And constant firefighting means nobody ever steps back to look at payment patterns or negotiate better terms.

Vendor segmentation: the foundation of intelligent AP

Segmentation changes everything. Instead of treating all vendors equally, you classify them based on operational importance, payment flexibility, and discount opportunities. Most businesses have three to five meaningful segments once you actually map it out.

Stop letting accounting slow your business down.

Acctaly automates your financial operations so you can focus on growth and compliance.

- Automated bookkeeping

- Real-time financial reporting

- Integrated tax management

No credit card required

Start with operational criticality. Raw material suppliers, essential software subscriptions, and payroll processors belong in Tier 1. These vendors can shut down operations if unpaid, so they get priority routing and faster approval workflows. A furniture manufacturer might put their lumber supplier, CNC machine leases, and shop insurance here.

Tier 2 covers important but flexible vendors — marketing agencies, non-critical software, professional services. Vendors you need, but who won't immediately impact operations if payment slips two weeks. These often offer the most flexibility on timing.

Tier 3 is everything else. Office supplies, barely-used subscriptions, one-off purchases. These can typically wait 45-60 days without consequences, freeing up cash for things that actually matter.

Segmentation doesn't stop at criticality, though. Layer in discount opportunities as a second dimension. That Tier 1 lumber supplier offering 2/10 net-30 terms moves into a "Priority Discount" segment. The marketing agency in Tier 2 with strict net-30 terms gets flagged differently than the one offering net-60.

Here's what a basic segmentation matrix looks like for a 30-person B2B services company:

| Vendor Segment | Examples | Payment Priority | Typical Terms | Routing Rule |

|---|---|---|---|---|

| Critical + Discount | Cloud infrastructure, Key contractors | Immediate if discount available | 2/10 net-30 | Auto-approve under $5k, expedited over $5k |

| Critical + Standard | Payroll, Insurance, Office lease | Within terms | Net-30 | Standard approval, never late |

| Flexible + Recurring | Marketing tools, Minor subscriptions | 35-45 days | Net-30 to Net-45 | Batch weekly, delay when cash tight |

| Flexible + One-off | Consultants, Event vendors | 45-60 days | Net-30 to Net-60 | Hold until cash positive |

| Low Priority | Office supplies, Meals, Minor expenses | 50-60 days | Net-30 | Batch monthly, pay when convenient |

This matrix becomes your routing engine. Every invoice that arrives gets classified and routed accordingly. No more manual decisions about who gets paid first.

Payment routing rules that actually work

Routing rules translate your segmentation into automated decisions. Instead of someone manually reviewing every invoice, the system knows exactly how to handle each vendor category.

The key is making rules specific enough to be useful but flexible enough to handle exceptions. A Critical + Discount vendor triggers an immediate payment workflow if the invoice arrives within the discount window. The system calculates whether taking the discount makes sense given current cash position and alternative uses of that capital.

Prefer rule thresholds tied to rolling cash metrics (e.g., 1.5x monthly burn) rather than fixed dates so routing adapts to real liquidity.

For a $10,000 invoice with 2/10 net-30 terms, the math is straightforward. Paying within 10 days saves $200. That's effectively a 36.5% annualized return on using cash 20 days early. Unless you're critically cash-constrained or have a higher-return immediate use for that $10,000, you take the discount.

Routing rules also handle the mundane decisions that eat up hours every week. All Tier 3 vendors automatically queue for payment at 55 days. Flexible recurring vendors get batched for weekly payment runs on Thursdays. Critical vendors trigger alerts if an invoice sits unapproved for more than 48 hours.

The rules also adapt to cash position. When cash drops below a set threshold — say, 1.5x monthly operating expenses — the system automatically shifts payment timing. Flexible vendors move from 35 to 50 days. Non-critical subscriptions pause. Only critical vendors and high-value discounts process normally.

Negotiation scripts that preserve relationships while extending terms

Most SMBs never negotiate payment terms because they assume vendors won't budge, or they don't want to come across as struggling. But vendors — especially B2B service providers — often prefer predictable payment at 45-60 days over uncertain payment at 30 days.

The conversation doesn't need to be complicated. For Tier 2 vendors where you have solid history, something like this works:

"We're standardizing our AP processes and moving established vendors like you to net-45 terms with guaranteed payment on day 45. This helps us manage cash flow predictably, and you'll know exactly when payment arrives every month. We can stick with net-30, but payment timing might vary between days 20-30 depending on our processing schedule. Which would work better for you?"

You're offering certainty in exchange for longer terms. Many vendors genuinely prefer knowing payment arrives on day 45 versus wondering if it'll be day 20 or day 35.

For larger vendors where you have some leverage, push harder:

"We're evaluating our vendor relationships for next year. You're currently one of three providers we're considering for [service]. The others offer net-60 terms with 2% early payment discounts. We prefer working with you, but we need comparable terms to justify continuing. Can you match net-60, or should we explore volume discounts instead?"

This positions the conversation as a business decision, not desperation. You're comparing options.

Document every negotiation outcome immediately. That marketing agency that agreed to net-45? Update their vendor record that day. The supplier that offered 2/10 net-60 on orders over $5,000? Build that into your routing rules. Without documentation, these wins disappear when the original negotiator leaves or vendors conveniently forget the agreement.

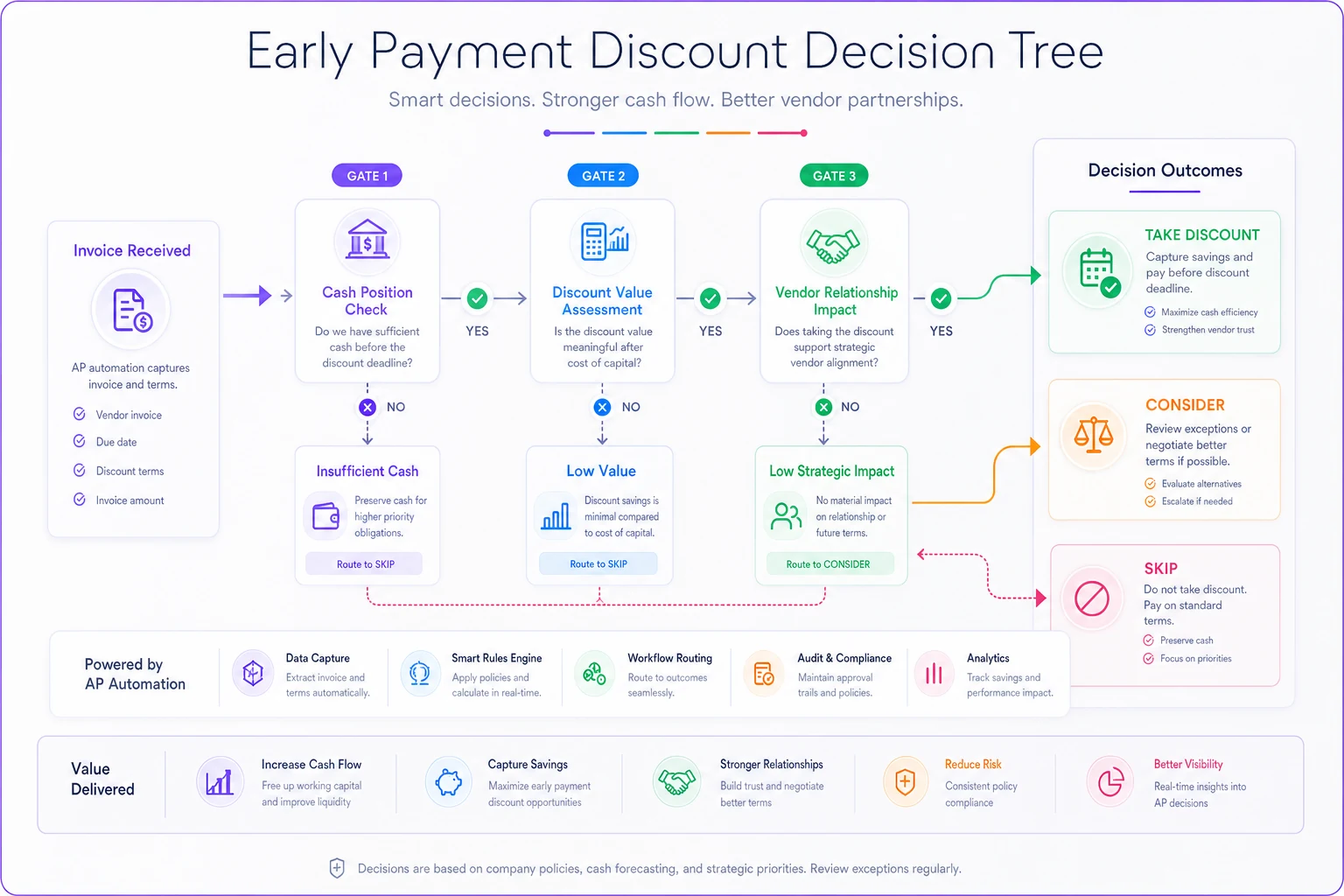

Decision trees for early payment discounts

Taking an early payment discount seems obvious — 2% savings is 2% savings. But working capital reality is messier. That $200 discount on a $10,000 invoice means nothing if paying early triggers an overdraft or forces you to delay payroll.

-

First gate

Cash position

- Current cash > 2x monthly expenses: Proceed to discount evaluation - Current cash between 1.5-2x monthly expenses: Only take discounts > 2.5% - Current cash < 1.5x monthly expenses: Skip all early payment discounts -

Second gate

Discount value

- Discount annualized return > 30%: Always take if first gate passes - Discount annualized return 20-30%: Take unless cash is needed within 30 days - Discount annualized return < 20%: Usually skip unless excess cash -

Third gate

Vendor relationship

- Strategic vendor with volume negotiations coming: Always take to build goodwill - Standard vendor with stable relationship: Follow gates 1 and 2 - Problem vendor with service issues: Skip discount, use it as leverage

In practice, this becomes automatic fairly quickly. Your accounting team knows that when cash is healthy, they capture all discounts above 2%. When cash tightens, only the highest-value ones process. The decision tree removes daily arguments about whether to take each discount.

A regional distributor automated this entire decision tree in their AP system. Invoices with early payment discounts route through the logic automatically — if the discount qualifies, payment schedules for the optimal date; if not, it routes to standard terms. They now capture roughly $18,000 annually in discounts they previously missed, without the cash crunches that came from overly aggressive discount capture before they had a system.

Automated approval workflows by supplier tier

Manual approval workflows kill cash flow optimization. The CEO reviews everything over $1,000, but they're traveling. The CFO approves marketing expenses, but they're in back-to-back meetings. Meanwhile, discount windows expire and vendor relationships strain.

Automated approval works differently. Instead of routing based solely on dollar amounts, you route based on vendor tier, expense category, and business context. Faster processing for critical vendors, appropriate oversight where it actually matters.

Tier 1 vendors get streamlined approval. If it's a recurring expense within 10% of the usual amount, it auto-approves. That $12,000 monthly inventory order doesn't need CEO sign-off every month. The system knows the pattern, validates it against the purchase order, and processes payment.

Tier 2 vendors follow category-based rules. Marketing expenses under $2,500 route to the marketing lead. Professional services under $5,000 route to the department head who engaged them. Only unusual amounts or expenses exceeding thresholds escalate to senior review.

Tier 3 vendors batch for weekly review. Instead of interrupting executives for every $50 expense, these accumulate for a single session. The reviewer sees all pending low-priority expenses and approves in bulk or flags specific items.

Here's how one 40-person SaaS company structures their automated approval matrix:

| Scenario | Tier 1 Vendors | Tier 2 Vendors | Tier 3 Vendors |

|---|---|---|---|

| Healthy Cash (>2x monthly burn) | Auto-approve up to $10k if recurring | Department head up to $5k | Batch approval weekly |

| Normal Cash (1.5-2x burn) | Auto-approve up to $5k if recurring | Department head up to $2.5k | Batch approval, flag >$500 |

| Tight Cash (<1.5x burn) | All require CFO approval | Require justification, CFO approval >$1k | Hold all except critical |

The system also handles exceptions. New vendors always require setup approval regardless of tier. Expenses exceeding 20% of historical average trigger review even for auto-approved vendors. International payments route through compliance review. These catch real problems without slowing down routine processing.

Implementation timeline and tracking metrics

Rolling out a working capital AP strategy takes roughly 6-8 weeks done properly. Not because the concepts are complex, but because you need historical data, vendor cooperation, and team buy-in to make it stick.

Weeks 1-2: Analysis and segmentation Pull six months of AP data. Identify your top 20 vendors by spend — these usually represent around 80% of your payables. Classify each by criticality and payment flexibility. Document current payment terms and historical payment timing. You'll find patterns quickly: vendors you consistently pay late without consequences, and others where even a day's delay triggers calls.

Weeks 3-4: Vendor negotiations Start with friendly Tier 2 vendors where you have good relationships. Test your negotiation scripts. Document every outcome. Most businesses successfully extend terms with 30-40% of vendors on the first pass. Don't push critical vendors yet — build confidence with the easier wins first.

Weeks 5-6: Build routing rules and approval workflows Turn your segmentation into specific rules. Even manual routing rules written on a checklist beat no system at all. The monthly close system you've built provides a natural checkpoint to review and adjust these rules over time.

Weeks 7-8: Training and refinement Train your team on the new workflows. Run parallel for a week — process invoices the old way and new way simultaneously to catch issues. Refine rules based on what breaks. Set up dashboards to track key metrics.

The metrics that matter:

-

Days Payable Outstanding (DPO) by vendor tier

Should increase for Tier 3, stay stable for Tier 1

-

Early payment discount capture rate

Target 90%+ for discounts meeting your criteria

-

Payment timing variance

Should decrease as routing rules standardize decisions

-

Vendor payment delays

Critical vendors should hit zero, others within agreed terms

-

Cash conversion cycle

Combined with receivables and inventory, should improve by 5-10 days

One wholesale distributor tracked these metrics after implementing tiered AP management. Their DPO increased from 31 to 43 days while early payment discount capture jumped from around 40% to 85%. The combined impact freed up roughly $200,000 in working capital — cash they reinvested in inventory that turned faster than their previous AP terms allowed.

Where AI automation transforms AP operations

This is where AI-powered operational software genuinely changes things for small businesses. Instead of manually classifying hundreds of invoices, training staff on complex routing rules, and constantly adjusting approval workflows, the platform handles it automatically.

Modern AP automation built for SMBs learns vendor patterns within weeks. It identifies which vendors consistently offer discounts, which ones accept delayed payment without complaint, and which ones need immediate attention. It suggests payment timing optimizations based on your actual cash flow forecast — not just rigid rules someone configured two years ago.

The negotiation support alone is worth it. The system tracks payment terms across all vendors, surfaces negotiation opportunities based on payment history, and can draft initial outreach. When you've been paying a vendor at 45 days who officially requires net-30, that's a conversation the system flags automatically. Most finance teams miss these entirely because nobody has time to audit vendor payment histories by hand.

The real value comes from connecting AP to broader financial operations. When integrated with your chart of accounts structure, the platform provides real-time visibility into expense categories and upcoming cash requirements. It knows when large receivables are coming in and can time payments accordingly, and it picks up seasonal patterns before you're already in a cash crunch.

Approval workflow automation eliminates the biggest bottleneck in most SMB finance operations. Instead of chasing approvals through Slack or email, the system routes invoices based on your rules, sends notifications when action is actually needed, and escalates when something unusual surfaces. An invoice running 50% higher than usual gets flagged automatically. The recurring software subscription processes without anyone touching it.

Building a working capital AP strategy for SMB operations isn't complex financial engineering. It's about treating different vendors differently, automating routine decisions, and capturing opportunities that are already hiding in your existing payables.

Most businesses can free up 10-20% of their working capital just by segmenting vendors and adjusting payment timing. Add consistent discount capture and better terms from negotiation, and you're looking at meaningful improvement without any additional revenue.

The businesses that struggle with AP aren't lacking intelligence or effort. They're managing modern payment complexity with startup-era processes. Every invoice gets the same treatment. Every payment decision happens in isolation. Every approval follows the same rigid workflow regardless of context.

The playbook here — vendor segmentation, payment routing rules, negotiation scripts, discount decision trees, and automated approvals — turns AP from a daily scramble into something that actually works in your favor. Cash stays in your account longer. Discounts get captured consistently. Vendors get paid predictably within agreed terms.

Start with segmentation. Even if you change nothing else, categorizing your vendors and treating them differently will improve your cash position within 30 days. Add routing rules and approval automation as you build confidence. Within two months, you'll wonder how you managed AP any other way.

The difference between businesses that constantly stress about cash and those that operate with confidence usually isn't revenue or funding. It's whether they've built systems that handle the fundamentals — and few fundamentals matter more than intelligently managing who gets paid and when.

Ready to take control of your finances?

Join over 2,000 businesses using Acctaly to simplify accounting, accelerate cash flow, and ensure tax readiness.