Most internal controls for small finance teams fail because they're built for companies that don't exist yet. You implement a four-person approval chain when you have six employees total. You require dual signatures on $200 purchases while $8,000 invoices auto-pay through your credit card. You build controls for fraud that might happen instead of errors that definitely will.

That disconnect creates more risk than having no controls at all. Employees bypass rigid systems and build shadow workflows. Exceptions become the norm. The controls you thought protected you turn into decorative checkboxes that everyone ignores.

Controls need to match your actual headcount, not your aspirational org chart. They need to prevent the mistakes your team actually makes, not the theoretical fraud you read about in audit textbooks.

Why traditional controls break at different team sizes

The control framework that works for a three-person finance team becomes actively harmful at ten people. What protects a ten-person team creates bottlenecks at fifty. Each growth stage needs fundamentally different control architecture.

At the smallest scale—one to three people in finance—your biggest risk isn't fraud. It's basic human error. Someone forgets to record a transaction. A decimal point shifts. An invoice gets paid twice because two people thought the other hadn't done it. Controls at this stage need to catch mistakes, not prevent elaborate schemes.

When you hit four to ten people, coordination becomes the primary failure point. Different people handle different parts of the same process. Information lives in multiple systems. The left hand genuinely doesn't know what the right hand authorized. Controls here need to create visibility across disconnected workflows.

By the time you reach ten to fifty people in finance, you face actual segregation of duties challenges. The person entering invoices shouldn't approve payments. The person booking revenue shouldn't control collections. But unlike enterprise companies with hundreds of finance professionals, you still need flexibility. Controls must prevent fraud while allowing operations to function when key people are out sick.

The 1–3 person framework: Error prevention over fraud detection

With a tiny finance team, every control adds friction. You can't afford complex approval matrices when the CFO, controller, and AP clerk are the same person. Focus on systematic error prevention instead.

Stop letting accounting slow your business down.

Acctaly automates your financial operations so you can focus on growth and compliance.

- Automated bookkeeping

- Real-time financial reporting

- Integrated tax management

No credit card required

Start with threshold-based exception reporting. Set up automated alerts for transactions that deviate from normal patterns—not because they indicate fraud, but because they're probably mistakes. An invoice 40% higher than the vendor's average? Flag it. A payment to a new account for an existing vendor? Review it. A journal entry that shifts account balances by more than 25%? Verify it.

Your approval matrix should be dead simple:

-

Under $500

No approval needed, but all transactions visible in daily summary

-

$500–$2,500

Email approval from owner or designated backup

-

Over $2,500

Documented approval with business justification

The key is making these controls systematic, not manual. Use banking rules to enforce payment limits. Set up automated emails for threshold breaches. Create standardized templates for common transactions. The goal is catching errors without piling on extra steps.

For this team size, focus controls on these high-error areas:

-

Duplicate payments (same invoice number, similar amounts to same vendor within 30 days)

-

Missing documentation (payments without attached invoices)

-

Unusual GL postings (new account combinations, round numbers over $1,000)

-

Bank reconciliation breaks (unmatched transactions over 5 days old)

When these four areas are covered systematically, you've handled the vast majority of what actually goes wrong at this scale. Everything else is noise.

The 4–10 person framework: Coordination and handoff management

Once your finance team grows beyond three people, your biggest risk shifts from individual errors to coordination failures. Multiple people touch the same processes. Information gets lost between handoffs. Assumptions about who did what create gaps.

At this size, implement role-based workflows with clear handoff points. Don't just assign responsibilities—define exactly when and how work transfers between people. The AP clerk processes invoices through coding, then assigns to the controller for approval, who releases to the CFO for payment authorization. Each handoff needs documentation.

Your approval matrix expands but stays practical:

-

Under $1,000

Department manager approval

-

$1,000–$5,000

Department manager plus finance manager

-

$5,000–$25,000

Above plus CFO or owner

-

Over $25,000

Board notification or documented owner approval

What matters more than the matrix itself: exception workflows. What happens when the normal approver is unavailable? Who can unblock a payment for critical operations? How do emergency purchases get retroactive approval? These aren't edge cases—they happen constantly, and if you don't build explicit paths for them, people improvise, and improvisation is where things go wrong.

Build explicit exception paths:

-

Designated backups for each approval level with documented delegation

-

Emergency approval process for time-sensitive payments (payroll, critical vendors)

-

Retroactive approval requirements with explanation documentation

-

Escalation triggers for patterns of exceptions

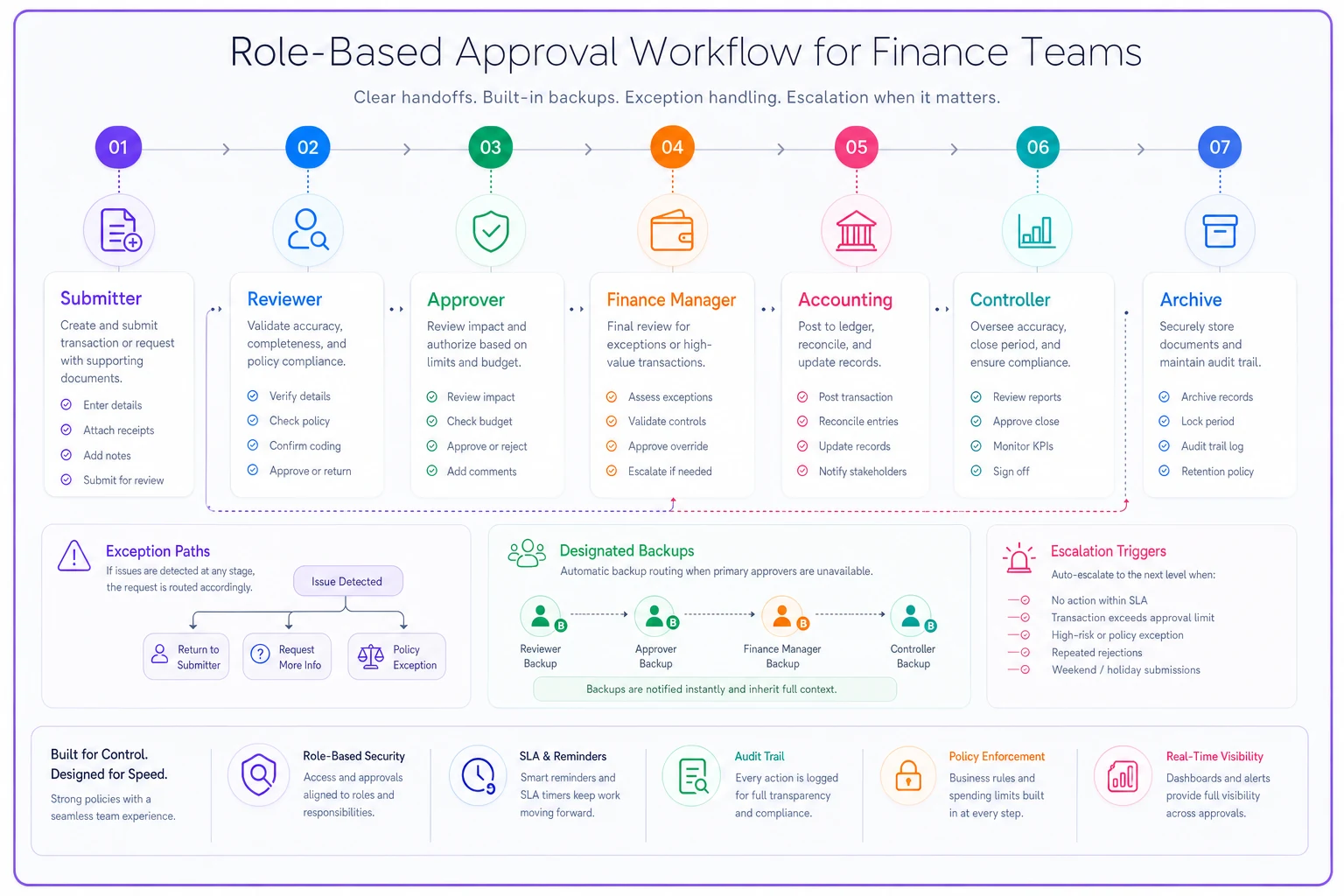

Here's a simple workflow to manage handoffs and exceptions.

Use this as a template to set handoff points and exception routing.

The 10–50 person framework: True segregation with pragmatic flexibility

At this scale, you need actual segregation of duties. But unlike large enterprises, you can't afford complete redundancy. Controls must prevent fraud while recognizing that your AP manager might also handle AR when someone's on vacation.

Implement compensating controls for necessary overlaps. If the same person must sometimes initiate and approve payments, require a documented review within 48 hours. If someone has system access beyond their normal role for backup purposes, log every transaction they perform outside their usual duties.

Your approval matrix becomes multi-dimensional:

-

Operating expenses follow standard dollar thresholds

-

Capital expenditures require additional technical approval

-

Vendor additions need verification regardless of amount

-

Contract changes trigger legal review above certain thresholds

-

New customer terms need sales and finance alignment

The real control power at this stage comes from systematic monitoring rather than trying to prevent every possible issue upfront. Build detection systems that catch problems quickly instead.

Weekly exception reports should cover: payments to new vendors, changes to vendor banking information, manual journal entries over $10,000, users accessing systems outside normal patterns, and approval patterns that deviate from policy.

Monthly control reviews should include sampling of transactions by type for documentation completeness, review of exception report responses, analysis of control override patterns, and verification of system access appropriateness.

The framework also needs built-in flexibility for business realities. Not every $5,001 purchase needs the same scrutiny. Build risk-based adjustments: trusted vendor fast-tracks for established relationships, pre-approved purchase categories with higher automatic thresholds, seasonal adjustments for predictable business cycles, and department-specific modifications based on operational needs.

Control effectiveness metrics by team size

Track different metrics depending on your team size to make sure controls actually work in practice.

| Team Size | Key Metrics to Track |

|---|---|

| 1–3 people | Error rate per 100 transactions; days to identify duplicate payments; % of transactions with complete documentation; time from invoice receipt to payment |

| 4–10 people | Handoff completion rate; approval cycle time by threshold; exception approval percentage; coordination error frequency |

| 10–50 people | Segregation violation incidents; detective control trigger rate; override pattern analysis; cross-training coverage percentage |

If you're not measuring these, you don't actually know whether your controls are working—you're just assuming they are.

The tooling stack that scales with headcount

Your control tools need to match your team size, not your aspirations. Overbuilding creates complexity that people bypass. Underbuilding leaves gaps that manual processes can't fill.

For 1–3 person teams, basic automation prevents most errors. Bank rules, simple approval emails, and automated reconciliation catch the majority of issues. You don't need enterprise GRC platforms—you need systematic error checking.

Integrate lightweight automation with your accounting system first to avoid shadow spreadsheets and manual reconciliations.

At 4–10 people, workflow tools become critical. Approval routing, shared queues, and audit trails prevent coordination failures. The investment in proper AP/AR software pays off through reduced errors and faster processing.

By 10–50 people, you need real control infrastructure. Role-based access systems, automated monitoring, and exception reporting become non-negotiable. But avoid enterprise solutions designed for thousands of users—they'll create more problems than they solve.

Red flags your controls don't match your size

Watch for these warning signs that your control framework doesn't fit your actual team.

Controls too heavy:

-

Routine payments regularly need emergency approval

-

People maintain "shadow" spreadsheets outside official systems

-

Exceptions happen more often than standard processes

-

Month-end close gets delayed by approval bottlenecks

Controls too light:

-

Same errors repeat across multiple months

-

Surprises appear during monthly close

-

Vendors complain about duplicate or missing payments

-

No clear ownership for specific control points

Both failure modes cost real money, just in different ways.

Building controls that grow with you

The framework you implement today needs migration paths for tomorrow. Design controls with growth triggers that adjust naturally as your team scales.

Going from three to four people shouldn't require rebuilding everything from scratch. Hitting ten people shouldn't mean replacing existing workflows—it should mean layering segregation requirements onto what already exists.

That means building modular controls from day one. Start with simple transaction monitoring that can add approval layers later. Implement basic documentation requirements that can expand into formal audit trails. Create role definitions that can split as headcount grows.

Most importantly, document the why behind each control. When you need to modify things for growth, understanding original intent prevents breaking critical protections while removing unnecessary friction. Skipping this step is how teams end up with nobody quite sure why a control exists, so nobody wants to touch it even when it's clearly causing problems.

The real cost of mismatched controls

Companies with controls that don't match their team size lose money in predictable ways. Too-heavy controls create workarounds that hide problems. Too-light controls miss expensive errors. Both scenarios cost more than properly-sized frameworks.

A ten-person finance team running enterprise controls might spend around 20% of their time on unnecessary approvals—essentially losing two full-time employees to friction. Meanwhile, a twenty-person team using controls designed for five people might lose 2–3% of revenue to errors and fraud, far exceeding what proper controls would have cost.

The solution isn't more controls or fewer controls. It's right-sized controls that match your actual operations. Build frameworks that prevent real risks your team faces, not theoretical risks from audit textbooks. As your chart of accounts scales with your business, your controls should scale with your team.

Practical next steps

Start by counting actual finance headcount—not titles, but people who touch financial transactions. Include part-time bookkeepers, fractional CFOs, and operational staff who approve purchases. That's your real team size.

Map your current controls against the framework for your size. Where do gaps exist? Where do you have unnecessary complexity? Fix the mismatches that create daily friction or repeated errors first.

Then build your migration trigger list. At what headcount will you add segregation? When will you implement formal approval routing? What growth milestone triggers a control review? Document these triggers now, before growth makes changes reactive instead of planned.

Internal controls for small finance teams succeed when they match reality, not theory. A three-person team needs different protections than a thirty-person team. The most sophisticated control is the one people actually follow—build for your reality, not someone else's ideal.

Ready to take control of your finances?

Join over 2,000 businesses using Acctaly to simplify accounting, accelerate cash flow, and ensure tax readiness.