Revenue leakage happens quietly. Your billing system reports $142,000 collected last month. Your general ledger shows $137,400 in recognized revenue. Your bank deposits total $139,850. Three different numbers, and somewhere between them, roughly $4,600 disappeared into operational gaps.

Most businesses only catch these discrepancies during month-end close—if they catch them at all. By then, the damage compounds. Failed charges that weren't retried. Partial payments sitting in suspense accounts. Refunds processed twice. Credits applied to wrong accounts. Each gap represents real money that should have hit your bank account but didn't.

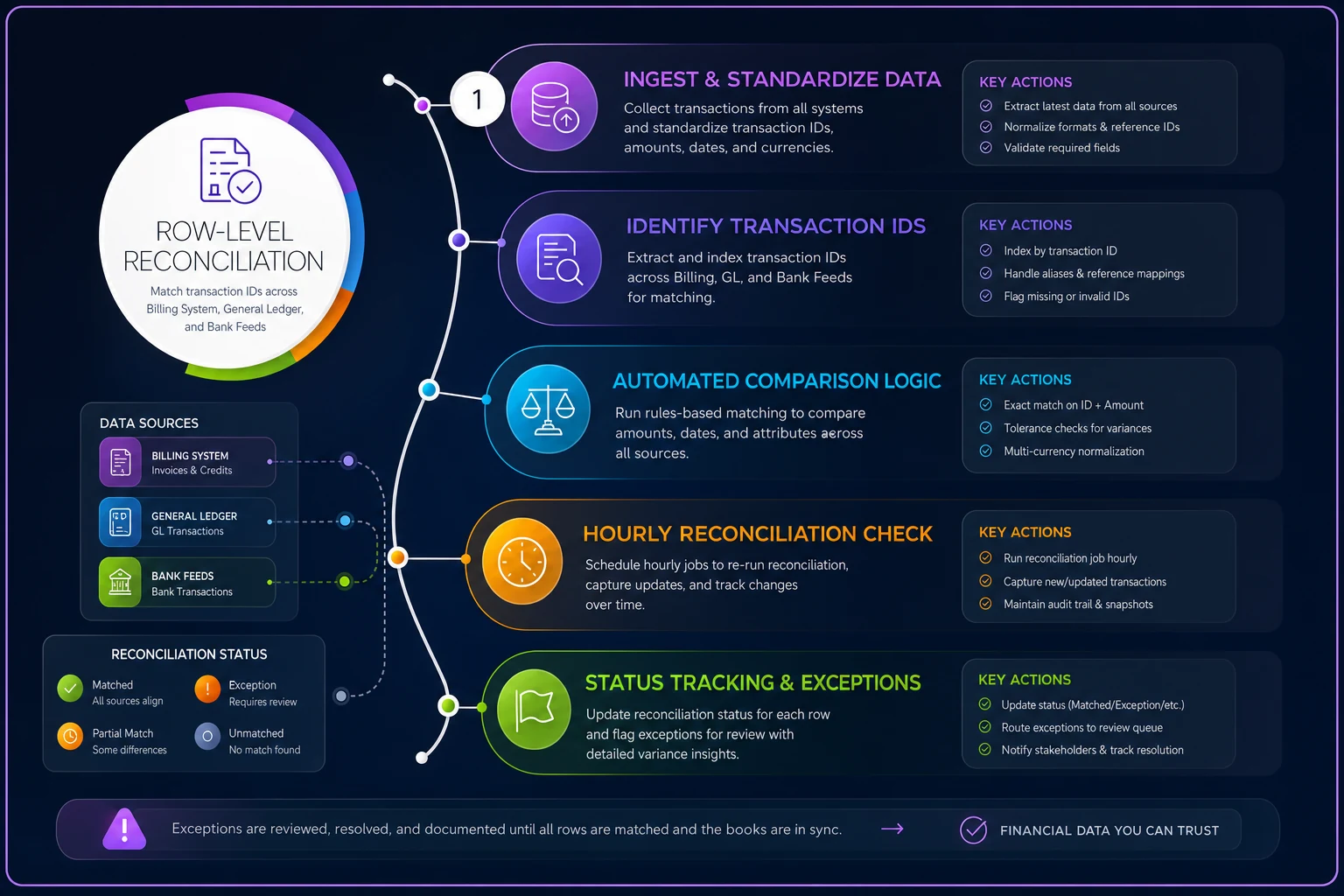

The fix isn't more manual checking. It's building systematic row-level reconciliation between your billing system, general ledger, and bank feeds—comparing individual transactions, not just totals. Setting up event-based audit rules that trigger when specific conditions occur. And creating clear remediation playbooks that match your team's actual capacity.

Why traditional reconciliation misses revenue gaps

Monthly reconciliation usually works like this: export billing summary, check against GL totals, verify bank deposits match. When numbers don't align, you dig through transactions trying to find the difference. This catches big errors but misses systematic leakage.

Consider what happens when a subscription platform processes 850 monthly charges. Maybe 12 fail initially. Your billing system retries 8 successfully over the next week. But 4 never process—they just sit there, marked as "pending retry" indefinitely. Your GL might show the full revenue (because the invoice exists), while your bank is missing those 4 payments entirely.

Or take marketplace businesses processing seller payouts. A $3,200 payout fails because of updated bank details. The system marks it failed, creates a liability entry, but never triggers a re-attempt. Your billing system shows the payout complete, your GL shows a growing liability balance, and the seller keeps asking where their money went.

These gaps multiply across payment methods. ACH returns that post 3-5 days later. Credit card disputes that reverse 45 days after the original charge. Wire transfers that get stuck in intermediary banks. Each creates a timing difference that traditional reconciliation assumes will "work itself out"—but often doesn't.

The real problem: most reconciliation focuses on proving totals match, not identifying which specific transactions need attention. You might know there's a $4,600 gap, but not which 23 transactions across 3 payment rails caused it.

Building row-level audit infrastructure

Row-level reconciliation means matching individual transactions across systems, not just comparing totals. This requires three things: consistent transaction identifiers, detailed status tracking, and automated comparison logic.

Stop letting accounting slow your business down.

Acctaly automates your financial operations so you can focus on growth and compliance.

- Automated bookkeeping

- Real-time financial reporting

- Integrated tax management

No credit card required

Start with transaction identifiers. Every charge, refund, payout, or adjustment needs a unique ID that travels between systems. Your billing system generates invoice #INV-2024-8394. When that posts to your GL, it needs to maintain that reference. When the payment hits your bank, the same ID should appear in the transaction description. Without this connection, you're manually matching amounts and dates—which breaks down fast when you have multiple $99 charges on the same day.

Next comes status tracking. A single customer payment might move through a dozen different statuses across its lifecycle:

| System | Status | What It Means | Action Needed |

|---|---|---|---|

| Billing | Initiated | Charge attempt started | Wait for processor response |

| Billing | Processing | Sent to payment processor | Monitor for timeout (5 min) |

| Payment Processor | Authorized | Card approved, not captured | Capture within 7 days |

| Payment Processor | Captured | Funds secured | Wait for settlement |

| Payment Processor | Settled | Sent to bank | Verify bank receipt (1-2 days) |

| Bank | Pending | Shown but not cleared | Wait for clearing |

| Bank | Posted | Funds available | Match to GL entry |

| GL | Unreconciled | Revenue recorded, not matched | Match to bank transaction |

| GL | Reconciled | Matched to bank | No action |

| Billing | Failed | Charge declined | Retry logic or customer contact |

| Billing | Refunded | Reversal processed | Verify GL adjustment |

| Billing | Disputed | Chargeback initiated | Provide evidence (7 days) |

Your reconciliation system needs to track where each transaction sits in this flow. One stuck in "Captured" for 5 days needs investigation. One marked "Failed" in billing but showing "Posted" in your bank means possible duplicate charges.

The comparison logic should run continuously, not just at month-end. Every hour, your system should:

-

Pull new transactions from billing system

-

Match against GL entries using transaction IDs

-

Verify against bank feed data

-

Flag mismatches for review

-

Trigger alerts for stuck transactions

-

Generate exception reports

This catches issues while they're still fixable. A failed ACH return spotted on day 2 can be re-run. Found on day 31, you might be out of luck.

Visualizing the flow makes it clear where to add automated checks and who should act when things get stuck.

Event-based triggers that actually detect revenue leakage

Static reconciliation tells you what already went wrong. Event-based monitoring catches problems as they happen. The key is setting triggers that detect revenue leakage patterns specific to your business model.

For subscription businesses, watch for these events:

Retry exhaustion: When a payment fails and your system exhausts retry attempts without success. Set a trigger after the final retry attempt that creates a task for manual intervention. One medical software company found 3% of their failed charges never entered retry logic at all—a specific error code their processor returned was simply getting ignored.

Partial payment acceptance: Customer pays $75 on a $100 invoice. System applies payment but doesn't flag the remaining balance. Trigger when payment amount is between 70-95% of invoice total—often indicates customer confusion about what's actually due.

Silent downgrades: Customer's payment method fails, system automatically downgrades their plan, but doesn't attempt to collect the difference. Trigger when account plan changes coincide with payment failure in the last 30 days.

For marketplace or platform businesses:

Held funds aging: Funds held for risk review that never get released. Trigger when held balance exceeds 7 days without a status change. One marketplace discovered $47,000 in funds held over 90 days that their risk system had never re-evaluated.

Payout failures without retry: Seller payout fails, system creates a liability, never attempts re-sending. Trigger when liability account balance for a single seller exceeds one standard payout amount.

Fee calculation mismatches: Platform fee calculated differently in billing vs GL. Trigger when fee percentage varies more than 0.1% from standard rate without an override reason.

For service businesses with complex billing:

Unbilled time: Time tracked in project system but never invoiced. Trigger when billable hours exist for more than 15 days without an associated invoice.

Credit memo loops: Credit issued, new invoice generated, credit re-applied repeatedly. Trigger when the same customer has more than 2 credits and invoices within 48 hours.

Contract rate mismatches: Service billed at wrong rate because contract updates didn't sync. Trigger when invoice rate differs from the contract rate in your CRM.

Setting the right thresholds matters a lot here. Start conservative—catching big issues first—then tighten as your team builds capacity to handle exceptions.

Concrete remediation playbooks mapped to team capacity

Solo operator or bookkeeper-only (1-2 people)

You can't investigate every small discrepancy. Focus on high-value, low-volume issues.

Daily (15 minutes):

-

Review transactions over $1,000 stuck in "pending" for 3+ days

-

Check for failed payouts over $500

-

Verify any manual refunds processed

Weekly (2 hours):

-

Run exception report for all mismatches over $100

-

Contact customers for failed payments over $200

-

Clear suspended transactions older than 7 days

Monthly (4 hours):

-

Full reconciliation of top 20% of customers by revenue

-

Pattern analysis on recurring failures

-

Adjustment entries for amounts under $100

Ownership: everything stays with the bookkeeper, escalating to the owner only for amounts over $5,000 or systematic issues affecting multiple customers.

Small finance team (3-5 people)

With basic specialization, you can catch more granular issues.

AP Specialist owns:

-

Vendor payout failures (daily check)

-

Credit memo applications (as they occur)

-

Refund processing verification (daily)

AR Specialist owns:

-

Failed payment retry management (2x daily)

-

Customer payment matching (continuous)

-

Dispute response coordination (as needed)

Controller/Senior owns:

-

Exception review over $500 (daily)

-

Pattern analysis and system fixes (weekly)

-

GL adjustments and write-offs (monthly)

Build in rotation for investigation tasks. Week 1: AR specialist investigates all mismatches. Week 2: AP specialist takes over. This prevents investigation fatigue and cross-trains your team at the same time.

Growing team (6-15 people)

At this scale, clear escalation paths become non-negotiable.

Level 1 (Junior staff): Investigate and resolve:

-

Mismatches under $250

-

Standard retry failures

-

Basic customer contact for payment updates

-

Flag patterns for review

Level 2 (Senior staff): Handle:

-

Mismatches $250-$2,000

-

Systematic issues affecting multiple transactions

-

Vendor/partner reconciliation

-

Process improvements

Level 3 (Manager/Controller): Own:

-

Mismatches over $2,000

-

Write-off decisions

-

System integration issues

-

Monthly pattern review with leadership

Create standard investigation forms. Every issue needs: transaction ID, amount, which system is showing the error, steps taken, and resolution or escalation reason. Over time, this builds real institutional knowledge about what breaks and why.

Alert thresholds that prevent false positives

Alert fatigue kills reconciliation programs faster than anything else. Your team starts ignoring notifications when every small timing difference triggers a flag. The solution is intelligent thresholds based on transaction patterns and business impact.

Start with time-based thresholds that match your payment rails:

Credit cards: Allow 3 business days between billing and bank posting before alerting. Normal settlement is 1-2 days, but weekends and holidays push that out.

ACH transfers: Wait 5 business days for matching. ACH can take 3-4 days normally, plus potential returns.

Wire transfers: Alert after 2 business days. Wires should be same-day or next-day at most.

International payments: Set 7-10 day thresholds depending on the corridor.

Layer in amount-based thresholds built around your revenue profile:

-

Alert immediately

Single transactions over $2,000

-

Alert daily

Cumulative mismatches over $1,000

-

Alert weekly

Individual mismatches $100-$1,000

-

Monthly review

Everything under $100

Adjust based on your margins. A 60% margin business can tolerate more investigation cost than one running at 15%.

Frequency patterns matter too. If a customer normally pays $500 monthly and suddenly you see three $500 charges in one week, that's worth a look even if each transaction appears normal on its own.

Start conservative with thresholds that protect cash first, then tighten them as your team proves capacity to handle exceptions.

Build in seasonal adjustments as well. Payment patterns shift during holidays, fiscal year-end, and industry-specific cycles. Your December thresholds might need to be different from your February ones.

The compound effect of systematic reconciliation

When you implement row-level reconciliation with proper alerts and playbooks, the impact compounds over time. Month one, you might find $4,000 in missing revenue. Month two, $2,800. By month six, you're catching issues before they become actual leakage.

A regional equipment rental company tried this approach after noticing unexplained variance between billing and bank deposits. First month revealed $8,200 in failed ACH transfers that were never retried—their system flagged them for manual review, but nobody was actually checking that queue. Second month turned up $3,400 in partial payments where customers paid deposit amounts instead of full invoices. By month four, they'd fixed their payment retry logic, clarified invoice formats, and dropped leakage to under $500 monthly on $180K revenue.

The bigger win was structural. Systematic reconciliation revealed a contract modification workflow that wasn't updating billing rates correctly—fixing that prevented roughly $2,000 monthly in under-billing going forward.

Patterns emerge that actually inform business decisions too. Maybe Tuesday payment runs have 3x higher failure rates because customers get paid Friday and spend over the weekend. Or invoices over $5,000 need different payment terms because they trigger additional approval workflows at customer organizations. You only see this stuff when you're tracking at the transaction level.

When AI-assisted platforms make sense for reconciliation

Manual row-level reconciliation works when you're processing dozens of transactions daily. Beyond that, the investigation burden overwhelms your team regardless of how good your playbooks are.

Modern operational platforms handle the matching logic automatically. They pull transaction data from your billing system, GL, and bank feeds, then use pattern recognition to match related transactions even when identifiers don't perfectly align. A charge for $1,000 that becomes a $980 deposit after fees gets matched automatically instead of firing as a discrepancy.

The real value comes from smarter exception handling. Instead of alerting on every mismatch, these systems learn your resolution patterns. If you consistently write off differences under $10 on international transactions, the platform starts auto-resolving those while still tracking them for reporting.

AI automation particularly helps with investigation workflows. Rather than manually checking three systems to understand why a transaction failed, automated platforms can trace the full lifecycle and surface a complete picture: "Payment of $750 failed at processor due to insufficient funds, retry scheduled for Friday, customer notified via email, no response yet."

Before switching systems though, make sure you've cleaned up your existing data. Migrating messy reconciliation processes just creates automated mess.

This becomes critical as transaction volume grows. A business processing 10,000 monthly transactions can't manually investigate 100 daily exceptions. But an AI-assisted platform can categorize those exceptions, auto-resolve the routine ones, and surface only the 10-15 that actually need human judgment.

For teams under 5 people, these platforms also provide coverage during absences. Your sole bookkeeper taking vacation shouldn't mean reconciliation stops for a week. Monitoring continues running, flagging only critical issues immediately while queuing routine items for their return.

Building reconciliation discipline that scales

The hardest part isn't technical—it's maintaining discipline as the business grows. What works at $100K monthly revenue breaks at $1M. The key is building practices that scale with complexity.

Start with clear ownership, even in small teams. "Everyone is responsible" means nobody is. Assign reconciliation ownership to specific people, with backup coverage defined. As you grow, that ownership shifts from individuals to roles to teams.

Documentation matters, but keep it simple. A one-page playbook that actually gets used beats a fifty-page manual that sits unread. Focus on: what to check, when to escalate, how to resolve common issues. Update quarterly based on new patterns.

Regular reviews prevent drift. Monthly, someone senior should ask: what patterns are we seeing? Which alerts fire most often? What manual processes could be automated? Without that review, exceptions slowly become normal and small leaks become floods.

Set escalation triggers based on cumulative impact, not just individual amounts. Ten $50 discrepancies might indicate a systematic issue worth more attention than a single $500 mismatch. Track both.

For SaaS businesses especially, this reconciliation discipline becomes critical for accurate revenue recognition. You can't recognize revenue you haven't actually collected, and deferred revenue for services not yet delivered needs its own tracking.

Connect reconciliation to business operations too. Sales needs to know about payment failures. Customer success should understand dispute patterns. Product teams benefit from knowing which payment methods have the highest success rates. Revenue leakage isn't just an accounting problem—it's an operational one.

Making reconciliation stick

Businesses that successfully eliminate revenue leakage share three traits: they catch discrepancies quickly, they fix root causes not just symptoms, and they maintain discipline even when things look fine.

Quick detection means daily reconciliation for significant transactions, alerts that fire within hours, and investigation workflows that begin immediately—not after month-end close.

Root cause fixing means asking "why" more than once. Why did that ACH transfer fail? Wrong account number. Why was it wrong? Customer updated it in the portal but it didn't sync to billing. Why didn't it sync? The integration breaks when account numbers contain dashes. Fix the integration, not just the individual transaction.

Maintaining discipline means running reconciliation even when everything looks clean. The month you skip because things have been matching perfectly is often the month a new issue starts compounding. Build it into your operational rhythm so skipping feels wrong, not so doing it feels like extra work.

Revenue leakage hides between systems, but it doesn't have to stay hidden. With row-level reconciliation, event-based monitoring, and clear remediation playbooks, you can find and fix the gaps that cost real money. Start with one high-value reconciliation point—maybe matching billing to bank deposits daily for transactions over $500. Build that discipline, prove the value, then expand. The money you recover pays for the effort multiple times over, and the operational insights you gain along the way prevent future leakage before it starts.

Ready to take control of your finances?

Join over 2,000 businesses using Acctaly to simplify accounting, accelerate cash flow, and ensure tax readiness.