The Fed's changing tone on rates caught my attention last week. Not because of the macro implications, but because of what happens next in the conference rooms and spreadsheets of hundreds of small businesses managing debt.

Recent Fed minutes show policymakers increasingly open to another rate hike, with inflation risks weighing heavier in their calculations. For SMBs carrying variable-rate debt or planning to refinance soon, this isn't abstract monetary policy—it's an immediate operational challenge.

The downstream effect nobody talks about

Most rising interest rates SMB finance discussions focus on the obvious: higher loan payments. But that's just the start of a cascade of operational adjustments that separates businesses that survive rate cycles from those that don't.

A regional logistics company I worked with nearly imploded during the last rate cycle. Not because they couldn't afford the extra $8,000 monthly on their equipment loans—they could. Their entire financial infrastructure assumed stable borrowing costs. Their forecasting models broke. Covenant calculations became useless. Cash conversion metrics stopped making sense.

They survived, barely, after rebuilding their entire financial reporting structure mid-crisis.

The businesses that navigated rate increases smoothly had something in common: flexible financial operations that could absorb variable inputs without breaking. They weren't necessarily more sophisticated—they just built their systems to handle change.

Why traditional SMB financial planning breaks in variable rate environments

Small business financial planning typically assumes tomorrow looks like today. Revenue projections extend current run rates. Expense budgets add inflation percentages. Cash flow models plug in fixed loan payments.

Stop letting accounting slow your business down.

Acctaly automates your financial operations so you can focus on growth and compliance.

- Automated bookkeeping

- Real-time financial reporting

- Integrated tax management

No credit card required

This works until a core assumption shifts.

Historical reporting becomes misleading. That debt service coverage ratio you've been tracking? It's based on yesterday's rate structure. Working capital trends assume predictable financing costs. Benchmark margins you use for pricing decisions bake in outdated interest assumptions.

Forward visibility disappears. Standard forecasting breaks when you can't predict a major expense line. Most SMB models treat interest as a fixed cost, like rent. When it becomes variable, the entire model needs restructuring—not just updating a cell in Excel.

Decision frameworks fail. Should you accelerate that equipment purchase before rates rise further? Lock in longer payment terms with suppliers even at higher prices? Pay down debt faster or preserve cash? Without updated decision models, these become guesses.

Building rate-resilient financial operations

Patterns emerge about who adapts successfully after watching businesses struggle through multiple rate cycles. It's not about predicting rates—nobody does that well. It's about building financial operations that function regardless of rate direction.

Start with scenario-based reporting structures

| Standard Reporting | Scenario-Based Reporting |

|---|---|

| Single P&L view | Multiple P&L scenarios (base case, +100bp, +200bp) |

| Historical cash flow | Cash runway at different rate levels |

| Fixed covenant calculations | Covenant headroom analysis under rate stress |

| Annual budget vs actual | Rolling forecasts with rate sensitivity |

| Static ROI calculations | Dynamic ROI with financing cost ranges |

A distribution company I worked with rebuilt their reporting this way. They discovered their "comfortable" 2.1x debt service coverage would drop to 1.4x with a 150 basis point increase—dangerously close to their 1.25x covenant threshold. This visibility let them renegotiate terms before rates moved, not during a crisis.

Restructure cash flow forecasting for uncertainty

Most SMB cash flow models are deterministic: revenue minus expenses equals cash. This breaks when a major expense becomes unpredictable.

-

Model your minimum cash position under worst-case rate scenarios, not average cases

-

Track cash conversion velocity weekly—how fast you turn sales into collected cash

-

Build payment flexibility into your operating cycle before you need it

-

Separate operational cash needs from debt service requirements in your planning

Cash flow management shifts from optimization (minimizing cash reserves) to resilience (maintaining flexibility).

Build a simple monthly worst-case cash runway that you update weekly so stress outcomes are always visible.

Implement dynamic covenant monitoring

Loan covenants typically include ratios like debt service coverage, debt-to-equity, or minimum EBITDA levels. These become moving targets when rates change.

Static covenant monitoring checks these quarterly, usually right before reporting to lenders. Dynamic monitoring tracks them continuously with forward projections.

Create a simple covenant dashboard that shows current position, 30-day trend, and projected position at different rate levels. Update it weekly, not quarterly. Share it with your leadership team, not just your CFO.

A specialty manufacturer avoided covenant violations by catching a trending decline six weeks before their reporting deadline. They had time to accelerate collections and defer non-critical capex, maintaining compliance without panic.

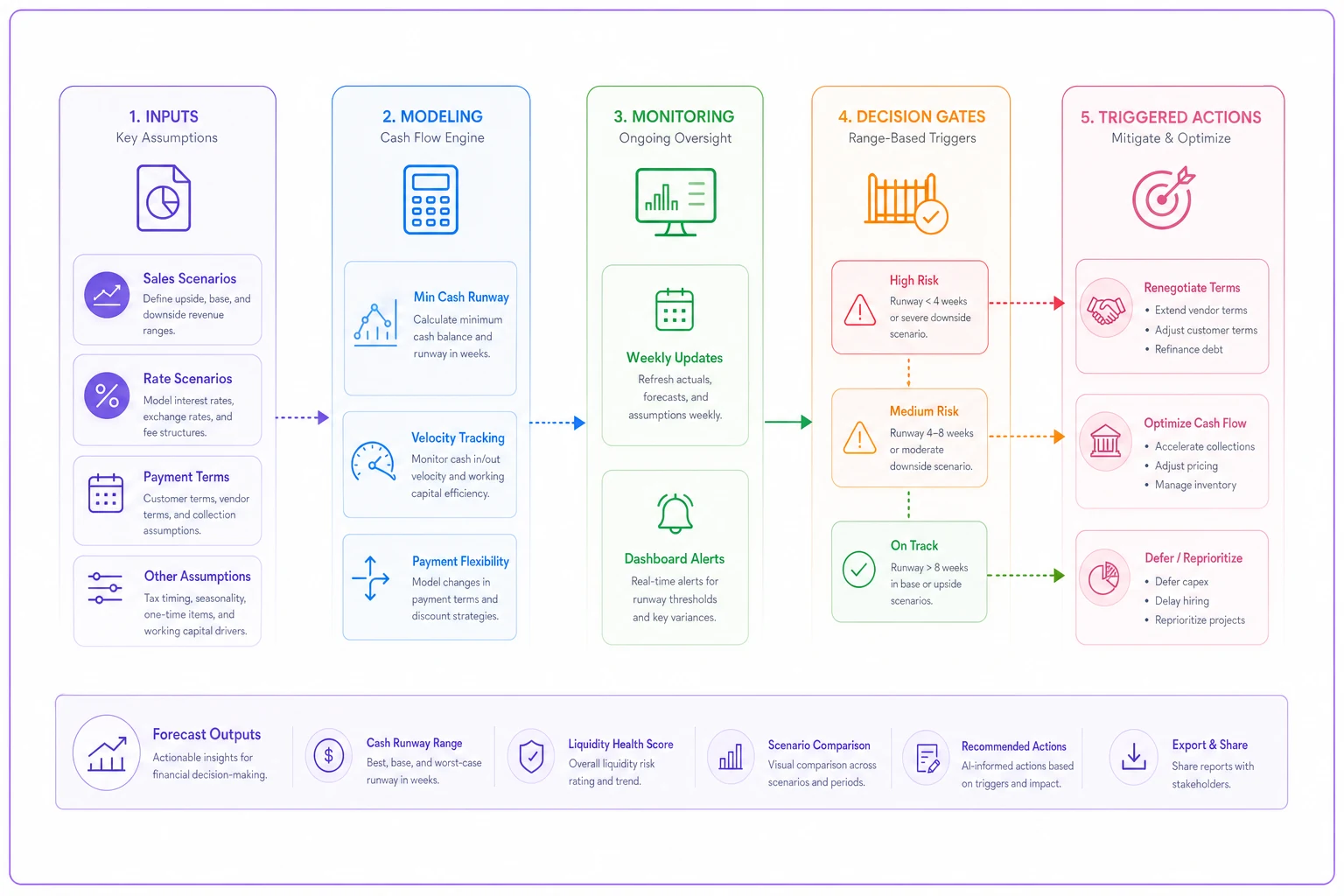

This workflow shows how to move from static cash plans to continuous scenario-driven monitoring that triggers operational responses.

The working capital trap in rising rate environments

Rising interest rates SMB finance challenges extend beyond loan payments into working capital management. Higher rates increase the cost of carrying receivables and inventory while making supplier financing more expensive.

The trap develops gradually. Companies maintain normal payment terms with customers while suppliers tighten credit. The gap strains working capital exactly when financing becomes costlier.

Smart operators flip this dynamic. They proactively renegotiate customer payment terms before liquidity tightens. They segment suppliers by payment flexibility, identifying who can extend terms versus who needs prompt payment. They reduce inventory levels strategically, accepting slightly higher procurement costs for dramatically lower carrying costs.

-

Moved their top 20% of customers to ACH payments with 2% early payment discounts

-

Negotiated extended terms with non-critical suppliers

-

Shifted from monthly to weekly inventory purchases for fast-moving items

-

Eliminated 60-day payment terms entirely

This freed up roughly $400K in working capital—equivalent to avoiding a $400K loan at rising rates.

When to actually lock in rates (and when to stay variable)

The reflexive response to rising rate fears is to lock in fixed rates immediately. This isn't always optimal.

Fixed-rate debt makes sense when you're financing long-term assets matching the loan term, your business has predictable cash flows, and the fixed rate premium stays under 150 basis points over variable. If your debt service coverage exceeds 2x even at the fixed rate, locking in provides stability.

Variable rates often work better when you expect to pay down debt quickly (under 24 months), your cash flows are seasonal, you have multiple financing options available, or you can operate profitably even with 200+ basis point increases.

A construction contractor kept variable rates on equipment financing but locked in fixed rates on their real estate. The equipment turned over every 2-3 years, making rate flexibility valuable. The real estate carried 15-year debt where rate certainty mattered more than minimizing cost.

Adjusting pricing and customer contracts for rate volatility

Most SMBs treat financing costs as back-office expenses disconnected from pricing. When rates rise, margins compress because pricing doesn't adjust.

Sophisticated operators build financing costs into pricing models, especially for projects with extended payment terms, contracts requiring working capital investment, and services with significant equipment financing components.

This doesn't mean adding a "rate adjustment charge." It means understanding your true cost to serve when financing costs change.

A commercial cleaning company restructured their contracts after rates increased. Instead of annual fixed-price agreements, they moved to quarterly pricing reviews tied to published indices. Clients accepted this because it was transparent and worked both ways—prices could decrease if rates dropped.

Creating operational buffers before you need them

Businesses that survive rate cycles build buffers during stable periods. Not just cash reserves—operational buffers that create flexibility.

Effective buffers include credit facility headroom (maintain 30-40% unused capacity on credit lines), vendor diversification to prevent single points of failure, contract flexibility with shorter commitment periods and adjustment clauses, and operational efficiency reserves—known cost reductions you haven't implemented yet.

Businesses that struggle in rising rate environments typically run at 95%+ efficiency during good times. No slack in the system means no ability to adjust when conditions change.

Beyond the spreadsheet: organizational readiness

Financial models and reporting systems matter, but organizational capability determines outcomes. Finance teams accustomed to stable conditions need different skills for variable rate environments.

Key capabilities that make the difference:

Scenario thinking over precision planning. Teams need comfort with ranges and uncertainty versus exact projections. This is surprisingly hard for finance professionals trained on precision.

Rapid decision-making with incomplete information. Rate environments change faster than perfect analysis allows. Better to make quick adjustments than wait for complete data.

Cross-functional coordination. Sales needs to understand how payment terms affect financing costs. Operations must grasp how inventory levels impact working capital. Without this coordination, finance operates in isolation.

External communication skills. Lenders, investors, and stakeholders need more frequent updates in volatile periods. Clear, proactive communication prevents surprise and maintains confidence.

The technology and tools question

Every financial challenge eventually leads to technology discussions. For rising interest rates SMB finance preparation, the tool question is less about what and more about how.

Spreadsheets can handle scenario modeling if properly structured. The limitation isn't calculation—it's maintenance and coordination. When multiple people need real-time visibility into dynamic scenarios, spreadsheet-based systems break down.

Purpose-built financial planning tools help, but implementation timing matters. Deploying new systems during crisis adds complexity when you need simplicity. The window for system upgrades is before rates move, not during.

Some operations benefit from AI-powered reporting frameworks that adapt to changing conditions. These platforms continuously update projections based on actual performance, reducing manual model maintenance. The operational value comes from freeing finance teams to focus on decisions rather than data management.

Technology is an enabler, not a solution. Strong operational discipline with basic tools beats sophisticated systems with poor processes.

The next 90 days: practical steps

Looking at recent Fed commentary, rate increases seem increasingly likely. For SMB finance teams, the next quarter represents a critical preparation window.

-

Run a rate stress test on your current debt. Add 100, 200, and 300 basis points to your variable rates. Calculate the monthly payment impact and annual cash flow effect.

-

Review all loan documentation for adjustment mechanisms. Understand exactly how rate changes flow through—some have caps, floors, or adjustment delays.

-

Model your covenant ratios at different rate levels. If any approach threshold levels, begin conversations with lenders now.

-

Accelerate working capital improvements. Every day saved in your cash conversion cycle reduces financing needs.

-

Document your current financial processes. When things speed up, you need clear procedures everyone understands.

-

Build simple scenario models for major decisions. Equipment purchases, expansion plans, and hiring decisions need rate sensitivity analysis.

-

Establish monitoring rhythms. Weekly cash flow reviews, monthly covenant checks, quarterly strategy adjustments.

Immediate priorities that actually move the needle should be concise, owned by a small cross-functional team, and reviewed at least weekly.

Moving forward with confidence

Rising interest rates create operational complexity for SMBs, but they're navigable with preparation. The businesses that struggle are those surprised by predictable consequences. The ones that thrive adapt their operations before crisis hits.

The difference isn't sophisticated financial engineering or perfect rate predictions. It's building financial operations flexible enough to handle uncertainty while maintaining strategic focus.

Strong businesses don't fear rate cycles—they prepare for them, adjust to them, and continue executing their strategy through them. The preparation work isn't particularly complex, but it requires intention and discipline to execute before conditions force your hand.

For SMB finance teams, the current moment offers an opportunity. Not to predict exactly what the Fed will do, but to build operational resilience that works regardless of their decision.

Ready to take control of your finances?

Join over 2,000 businesses using Acctaly to simplify accounting, accelerate cash flow, and ensure tax readiness.